Indices Climb to Highs as Breadth Quietly Thins

U.S. equities ground higher into Friday's close on AI-semiconductor leadership and an Iran-hope rally (Hormuz still closed), but only 11% of stocks sit in bullish stages, leaving the rally narrower than the tape suggests.

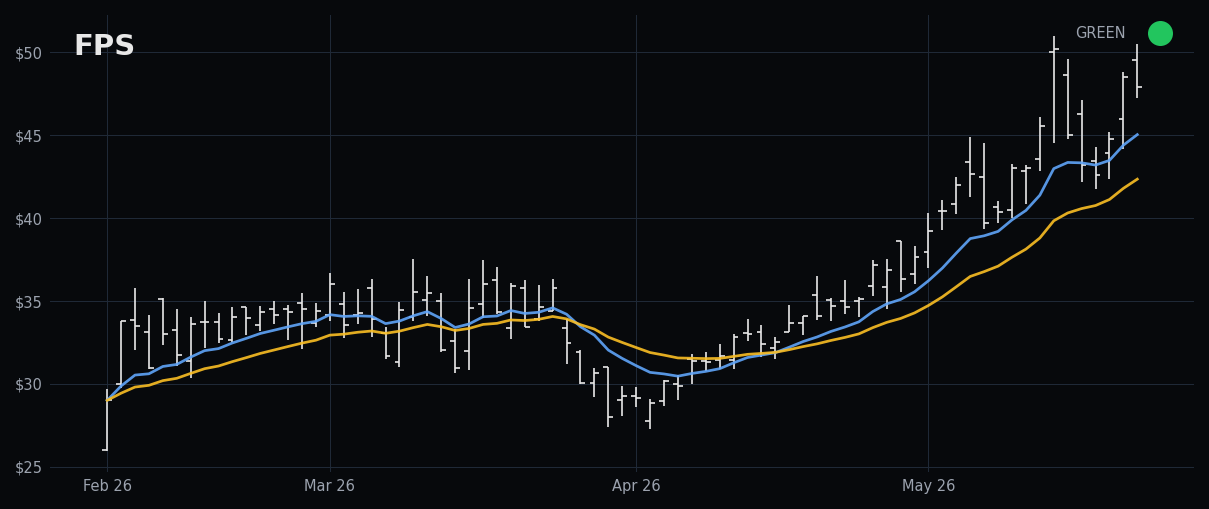

CMRF Phase: GRÜN

What Happened This Week

- Regime flipped GELB → GRÜN on Friday at composite +3; T2108 expanded 43% → 52% on the week.

- Macro stays heavy: inflation expectations jumped to 4.8%, Fed repricing toward "higher for longer" pushes rate cuts off the table.

- Only 11% of stocks in bullish Stages 1+2 — the indices are doing the work, the median name is not.

The week opened in a defensive crouch. T2108 began Monday at 43.4% with bond yields climbing and oil bid on Strait of Hormuz headlines, prompting our desk to hold the GELB regime and confine activity to A-grade EMA-crossback and 4B-minus pullbacks. Breakouts were locked out for four consecutive sessions as Deepvue's yield warnings and VolumeLeaders' breadth caution converged on the same message: structurally intact, tactically fragile.

By Wednesday, energy names — STRL, DINO, GLNG, CVI, LBRT — were doing most of the constructive work on the screener as crude held near triple digits. Thursday's quantum-computing headlines around reported federal equity stakes in IonQ and Rigetti briefly skewed sentiment bullish, but the morning note flagged the theme-rotation risk: hype without breadth confirmation tends to print fake signals. T2108 expanded to 51% with a +7.7% weekly change, enough to soften the posture without confirming a green light.

Friday brought the regime flip to GRÜN at a composite score of 3, restoring STANDARD_MODE with full 80% exposure and all entry types unlocked. The internals remain mixed: T2108 at 52.2% (+8.8 on the week), 54% of names above the 50-day, VIX at 16.8, only five distribution days — but Stage 1+2 participation at just 11% and a 4%-up ratio of 0.0 underline that the indices are doing the heavy lifting, not the median stock. Pick performance reflected that asymmetry: 35 of 40 setups realized, 33.3% accept hit rate, average return on accepts of 1.52%.

Markets rallied on dual catalysts: headlines suggesting the U.S. and Iran are making progress toward ending the war and reopening the Strait of Hormuz, plus another powerful leg in AI-linked semiconductors driven by upside earnings and guidance. However, beneath the surface, U.S. consumer sentiment hit an all-time low of 44.8, one-year inflation expectations jumped to 4.8%, and oil remains volatile around triple-digit levels with the Strait of Hormuz effectively closed. Bond markets are repricing Fed policy toward 'higher for longer' with rate cuts pushed off the table.

Index Snapshot

| Index | Last | Pivot | Support | VL Flow |

|---|---|---|---|---|

| SPY | $745.64 | $742.50 | $743 / $742 | $7.27B institutional inventory zone @ $742–743 per VolumeLeaders. |

| QQQ | $717.54 | $714.50 | $714.50 | $3.24B support cluster around $714.50 — break signals deeper pullback. |

| IWM | $285.12 | $280.10 | $280.10 | Holding above $280.10 accumulation keeps the small-cap broadening thesis intact. |

SPY $745.64 · Pivot $742.50 · Support $743 / $742

$7.27B institutional inventory zone @ $742–743 per VolumeLeaders.

QQQ $717.54 · Pivot $714.50 · Support $714.50

$3.24B support cluster around $714.50 — break signals deeper pullback.

IWM $285.12 · Pivot $280.10 · Support $280.10

Holding above $280.10 accumulation keeps the small-cap broadening thesis intact.

Sector Rotation & Bull-Snorts

Sector rotation was the week's clearest tell. The heating list — MultiUtilities, Passenger Airlines, Industrial Conglomerates, Aerospace & Defense, Electric Utilities — reads defensive; the drop-outs (Software, Construction & Engineering, Consumer Staples Distribution, Leisure Products) confirm leadership thinning at the top. VolumeLeaders' read backs this up: value and small caps outperformed growth on an eight-week SPX winning streak, with roughly 72.7% of S&P names above their 5-day MA — consistent with a defensive-to-cyclical handoff rather than a fresh tech leg, even as Qualcomm, AMD and NXP printed 3-11% single-session moves.

| Group | Mo → Fr | Δ | |

|---|---|---|---|

| MultiUtilities | #59 → #20 | +39 | |

| Passenger Airlines | #46 → #10 | +36 | |

| Industrial Conglomerates | #58 → #30 | +28 | |

| Aerospace & Defense | #63 → #37 | +26 | |

| Electric Utilities | #62 → #38 | +24 | |

| Retail REITs | #40 → #16 | +24 |

| Group | Mo → Fr | Δ | |

|---|---|---|---|

| Software | #8 → #22 | -14 | |

| Consumer Staples Distribution | #12 → #23 | -11 | |

| Construction & Engineering | #15 → #24 | -9 | |

| Leisure Products | #17 → #26 | -9 |

Bull-Snorts

Next Week

Next week is bookended by earnings risk and a single high-stakes macro print. CRM and COST report Wednesday and Thursday AMC respectively, with MOD (Tuesday AMC), AMSC and HQY filling out the calendar — enough single-name volatility to test the freshly minted GRÜN regime without confirming it. The week then closes Friday 29 May with the PCE release at 08:30 ET, the cleanest read on whether the bond market's 'higher for longer' repricing is justified. With breadth still thin under the surface, the asymmetry favors letting the data come to the tape rather than front-running it.

Calendar — Next Week

- 2026-05-25 — Markets closed (Memorial Day)

Macro releases

- 2026-05-29 (08:30 ET) — PCE Release

Earnings (tickers in our universe + S&P top-30)

- 2026-05-26 AMC — MOD · EPS est. 1.55 — exited pre-earnings 2026-05-22 (+9.54%)

- 2026-05-27 AMC — AMSC · EPS est. 0.10

- 2026-05-27 AMC — CRM · EPS est. 3.13

- 2026-05-28 AMC — HQY · EPS est. 1.11

- 2026-05-28 AMC — COST · EPS est. 4.92

Risk Watch

- Oil > $105 → tighten energy stops to 1×ATR (Hormuz still closed, oil holds above $100)

- 10Y > 5.0% → reduce growth exposure (Fed repricing higher-for-longer as inflation expectations rise)

- T2108 < 40% → halt new entries, drop to GELB-mode (leadership still narrow, breadth dimension at −1)

Key Takeaways

- Regime flipped to GRÜN Friday, but Stage 1+2 participation only 11%.

- Rotation into utilities, airlines, defense; software dropped from top twenty.

- PCE on 29 May and CRM/COST earnings define next week's risk.

Pick Performance

- Accept: 12 realized · 3 pending

- Watch: 23 realized · 2 pending

- Total: 40 setups · Hit-Rate (Accepts): 33.3% · Avg: +1.52%

Spotlight — Methodical Read

Full Pick Book

| Date ↓ | Ticker | Verdict | Entry | Exit | Return |

|---|---|---|---|---|---|

| 2026-05-22 | MNST | Accept Full | — | — | not-yet |

| 2026-05-22 | SBLK | Accept Probe | — | — | not-yet |

| 2026-05-22 | LRCX | Accept Probe | — | — | not-yet |

| 2026-05-21 | DVA | Accept Full | $199.93 | $198.52 | -0.71% |

| 2026-05-21 | UNFI | Accept Full | $49.82 | $49.31 | -1.02% |

| 2026-05-21 | NEO | Accept Probe | $9.11 | $9.23 | +1.32% |

| 2026-05-20 | CVI | Accept Full | $33.98 | $32.45 | -4.50% |

| 2026-05-20 | LBRT | Accept Full | $32.29 | $31.84 | -1.39% |

| 2026-05-20 | UNFI | Accept Probe | $49.35 | $49.31 | -0.08% |

| 2026-05-19 | STRL | Accept Full | $744.57 | $732.94 | -1.56% |

| 2026-05-19 | DINO | Accept Full | $71.82 | $69.91 | -2.66% |

| 2026-05-19 | GLNG | Accept Full | $56.64 | $52.36 | -7.56% |

| 2026-05-18 | MOD | Accept Full | $237.84 | $260.52 | +9.54% |

| 2026-05-18 | POWL | Accept Full | $260.41 | $279.22 | +7.22% |

| 2026-05-18 | BE | Accept Probe | $252.79 | $302.49 | +19.66% |

One report per week. No noise.